Berlin, February 25, 2026

[Update May 13, 2025

Urgewald will adjust the PAB assessment of Enel SpA in an upcoming data update based on newly available information.

According to our PAB methodology, we classified Enel as above the utility threshold based on the following information: According to Enel’s Annual Report 2024, the company derives 58,9 % of its revenue from its own electricity generation (p.466, Note 9a). For the fiscal year 2024, Enel reports the following scope 1 GHG emission intensity: 101 gCO2eq/kWh (AR 24 p.24).

Enel has recently published its AR 2025. For the fiscal year 2025, the company now reports a scope 1 GHG emission intensity of 97 gCO2eq/kWh (AR 25 p.39), which leads to the company dropping below the 100 gCO2eq/kWh threshold.

We inform you about this change because it affects the figure on PAB-critical investments communicated in our study “Finally Fossil Free” from February 2026. As underlined in the report, holdings in Enel SpA contributed 1,4 billion of the 1,9 billion of PAB-critical investments we identified in ESI Funds based on the available data at the time of research.]

A new study by Finanzwende and Urgewald in cooperation with Facing Finance shows: The naming guidelines introduced by the European Securities and Markets Authority (ESMA) in May 2025 led to more transparency and fewer fossil investments in funds carrying ESG-related terms in their names. However, many providers remain heavily invested in coal, oil and gas by strategically renaming their funds.

The full report is available here: https://www.urgewald.org/en/esg-fossil-free

For funds with terms such as "environment", "sustainable" or "impact" in their names ("ESI funds"), the ESMA guidelines set minimum standards for fossil investments. The study shows that many fund providers responded with the targeted renaming of funds, which allowed them to retain fossil investments worth €11.4 billion, or more than 60 percent of the investments originally affected. In some cases, they chose ‘soft’ terms such as "screened" or "advanced", which can also imply a certain level of sustainability but fall outside the scope of the new ESMA guidelines.

At the same time, ESI funds still retain €1.9 billion euros* of fossil investments that should have been sold under the new rules according to our analysis. This should prompt national supervisory authorities to effectively monitor compliance with the ESMA guidelines and ensure their consistent implementation across Europe.

Figure 1: How "ESI funds" have reacted to the ESMA guidelines

Magdalena Senn, sustainable financial markets officer at Finanzwende, says: "The ESMA guidelines have separated the wheat from the chaff when it comes to sustainable investments. Consumers can now find their way around the ESG market much better than before. However, the large-scale creative renaming of funds shows that this step is not enough to future-proof the European ESG market. We are also concerned about the fossil investments that remain in 'sustainability' funds. This shows that rules alone will not suffice. We also need supervisory authorities that consistently fulfill their mandate and monitor compliance closely."

Co-author Julia Dubslaff, financial analyst at Urgewald, adds: "Demand for sustainable investment products remains strong. Accordingly, the incentive for fund managers to offer such products is high. Our study shows: Asset managers use existing loopholes to hold on to fossil fuel investments. Since fund managers seem to have little intrinsic motivation to act sustainably, policymakers and regulators must establish clear and future-proof guidelines."

SFDR 2.0: An opportunity for more transparency – or a new greenwashing trap?

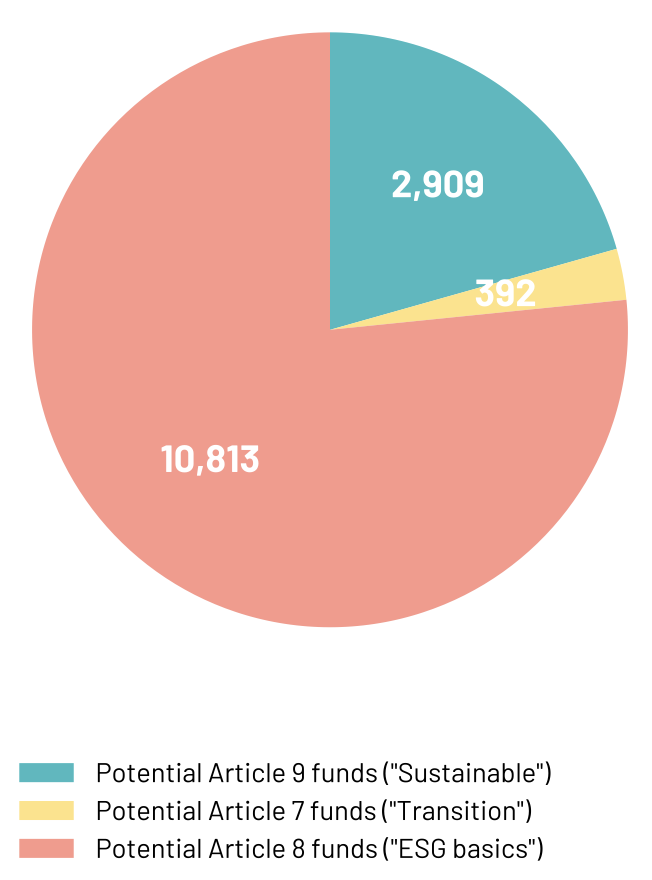

In a second step, the study analyzes the EU Commission's proposal to revise the Sustainable Finance Disclosure Regulation (SFDR 2.0). The SFDR provides a framework for ESG funds on the European market. Its current revision aims to further reduce greenwashing in the space. The EU Commission's proposal introduces three new fund categories. The categories "Sustainable" (Article 9) and "Transition" (Article 7) establish robust exclusions for companies active in the fossil fuel sector and – for the first time – also target companies engaged in fossil fuel expansion. Funds in the "ESG basics" category (Article 8), on the other hand, will only have to exclude certain coal companies.

Based on the current names of ESG funds, the study assumes which of the three new categories they would likely be classified under in the future. The results show: Funds that are likely to classify under the "Sustainable" category would have to sell an additional €2.7 billion in fossil investments. In the "Transition" category, €2.3 billion euros in fossil investments would need to be divested. This would represent a significant improvement for the credibility of current ESG funds. However, the "ESG basics" category risks becoming a new greenwashing trap: Over €100 billion – the vast majority of fossil holdings in current ESG funds – could remain invested in companies that are pursuing fossil fuel expansion projects or lack a Paris-aligned coal exit date.

Figure 2: Potential distribution of Art. 7, 8, 9 funds under SFDR 2.0 (number of funds)

Fiona Hauke, co-author and expert on financial regulation at Urgewald, says: "The revision of the SFDR could be a milestone for credible sustainable financial products. For this to succeed, however, the blind spot that the ‘ESG basics’ category represents needs fixing. The term ‘ESG’ clearly conveys a sustainability claim to consumers. The mandatory exclusion of fossil fuel expansion must also apply to the ‘ESG basics’ category. Fossil fuel expansion is incompatible with a stable climate and has no place in any fund marketed with environmental or sustainability claims."

Demands towards policymakers and supervisory authorities

- National supervisory authorities must effectively monitor compliance with the ESMA naming guidelines and ensure consistent implementation across Europe.

- EU policymakers must ensure that fossil fuel expansion is excluded from all future SFDR categories – including "ESG basics".