Berlin, January 27, 2026

Today, Urgewald and 13 partner organizations released the 2026 Metallurgical Coal Exit List (MCEL), the most comprehensive public database tracking companies expanding their met coal mining activities.

MCEL 2026 can be downloaded at coalexit.org/MCEL

Key Findings

- MCEL 2026 identifies 145 parent companies and around 200 subsidiaries worldwide that are expanding their metallurgical coal mining activities.

- 273 metallurgical coal expansion projects are planned or under construction, in over 20 countries.

- These projects represent 580 million tons per year of planned new and expanded capacity.

The data exposes a widening contradiction at the heart of the sector: while demand for metallurgical coal is forecast to decline this decade, companies are still accelerating plans to expand supply. If realized, these projects would increase global annual met coal production by 52%, risking a wave of high carbon assets that may never pay back.

Metallurgical coal is mainly used in traditional blast furnace steelmaking, one of the most emissions-intensive industrial processes still operating at a global scale. Coal-based steel production remains a major driver of climate pollution, accounting for around 11% of global CO2 emissions.

Metallurgical coal expansion is not just a problem on paper. It is already tearing into landscapes, waterways, and wildlife habitats, with devastating consequences for people and nature. From Queensland, where new open cut coal projects threaten fragile bushland ecosystems and endangered koalas, to Canada’s Elk Valley, where mining pollution has been linked to fish with deformed skulls and twisted spines, the impacts are immediate and lasting.

Communities living downstream of these mines are left with contamination risks that can stretch for decades, while companies keep pushing ahead with new projects that would lock in destruction long after the world has begun moving away from coal-based steel.

The growing relevance of this issue is reflected in the Science Based Targets Initiative’s newest Net-Zero Standard for Financial Institutions. The standard now explicitly recommends the exclusion of metallurgical coal developers, referencing MCEL.[1] Only one year after the dataset was first published, more than 150 financial institutions use MCEL to monitor and manage their exposure to metallurgical coal. Just this month, one of Finland’s largest pension funds, Ilmarinen, announced to divest from all met coal developers.[2]

In response to the findings, Lia Wagner, met coal expert at Urgewald, said:

“Green steel is no longer a future promise. It is here, it works, and is increasingly economically compelling. That makes new metallurgical coal mines a dead end. Financial institutions and policymakers must act now as there is no credible case for further expansion of metallurgical coal.”

About the Metallurgical Coal Exit List (MCEL)

The Metallurgical Coal Exit List (MCEL) is the world’s most comprehensive public database of met coal developers. It was designed to bring transparency to a sector that is often overlooked in the decarbonization process. As a sister database to the Global Coal Exit List (GCEL), MCEL enables financial institutions to better understand their exposure to this high-emissions industry and to develop new met coal exclusion policies. To ensure that our data creates lasting added value, MCEL is updated annually.

Is Metallurgical Coal Past Its Prime

The met coal industry is entering a decisive decade. While demand forecasts point downward, MCEL 2026 shows that companies are still planning major expansion, deepening the gap between market reality and industry strategy.

The newest coal report of the International Energy Agency (IEA) makes clear that building more metallurgical coal capacity is the wrong path: “Looking ahead, global met coal demand is forecast to decline gradually from 1,114 Mt to 1,061 Mt by 2030.”[3]

This would represent a reduction of around 53 million tons per year, equivalent in scale to the complete shutdown of metallurgical coal production by Glencore, BHP, Whitehaven and Exxaro Resources.[4] The decline is driven by structural shifts in steelmaking alongside slower industrial growth.

“Metallurgical coal appears to have already passed its peak.” – Lia Wagner, Met Coal Expert Urgewald

The 2026 MCEL data shows that China ranks second in metallurgical coal expansion (Figure 2). Yet the IEA report offers a note of hope: nowhere is met coal demand expected to decline more than in China.

Despite massive investments in metallurgical coal, China appears to recognize that the future of steel will be green. Last year marked a significant step when the country officially expanded its national Emissions Trading Scheme to cover the cement, steel, and aluminium sectors.[5]

Demonstrating this shift in practice, China exported steel made with green hydrogen rather than met coal to the EU for the first time last summer.[6]

The demand outlook is also shifting across other major markets. Europe, Japan, and Korea are facing declining demand for met coal. However, India and Indonesia are bucking this trend, with demand expected to rise.[7]

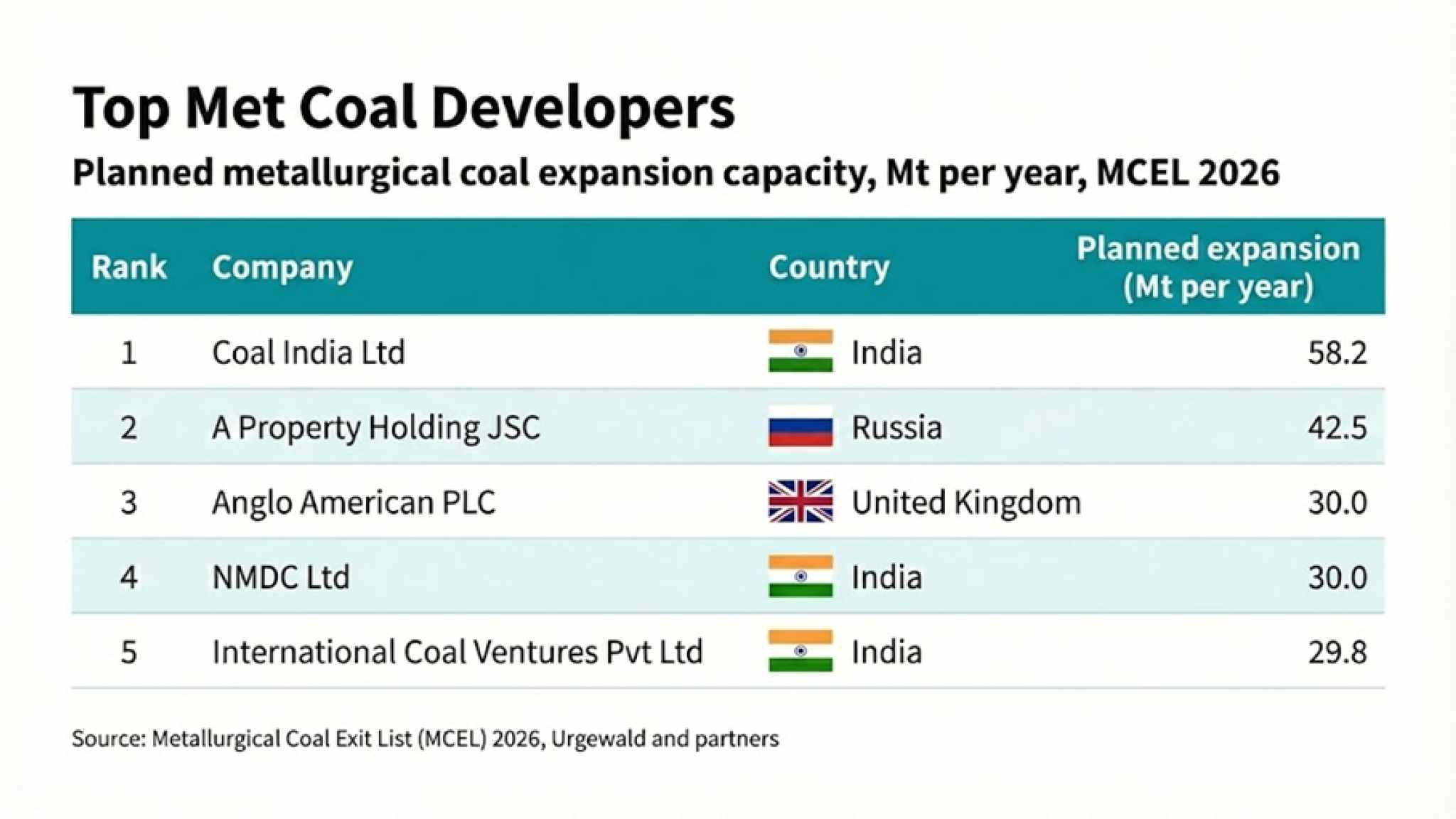

Therefore, it does not come as a surprise that three of the top five met coal developers are headquartered in India.

Figure 1: Top met coal expansion developers. Planned metallurgical coal expansion capacity (Mt per year) for the 5 leading developers identified in MCEL 2026. Source: MCEL 2026, Urgewald and partners.

Signs of Strain in Australia’s Metallurgical Coal Sector

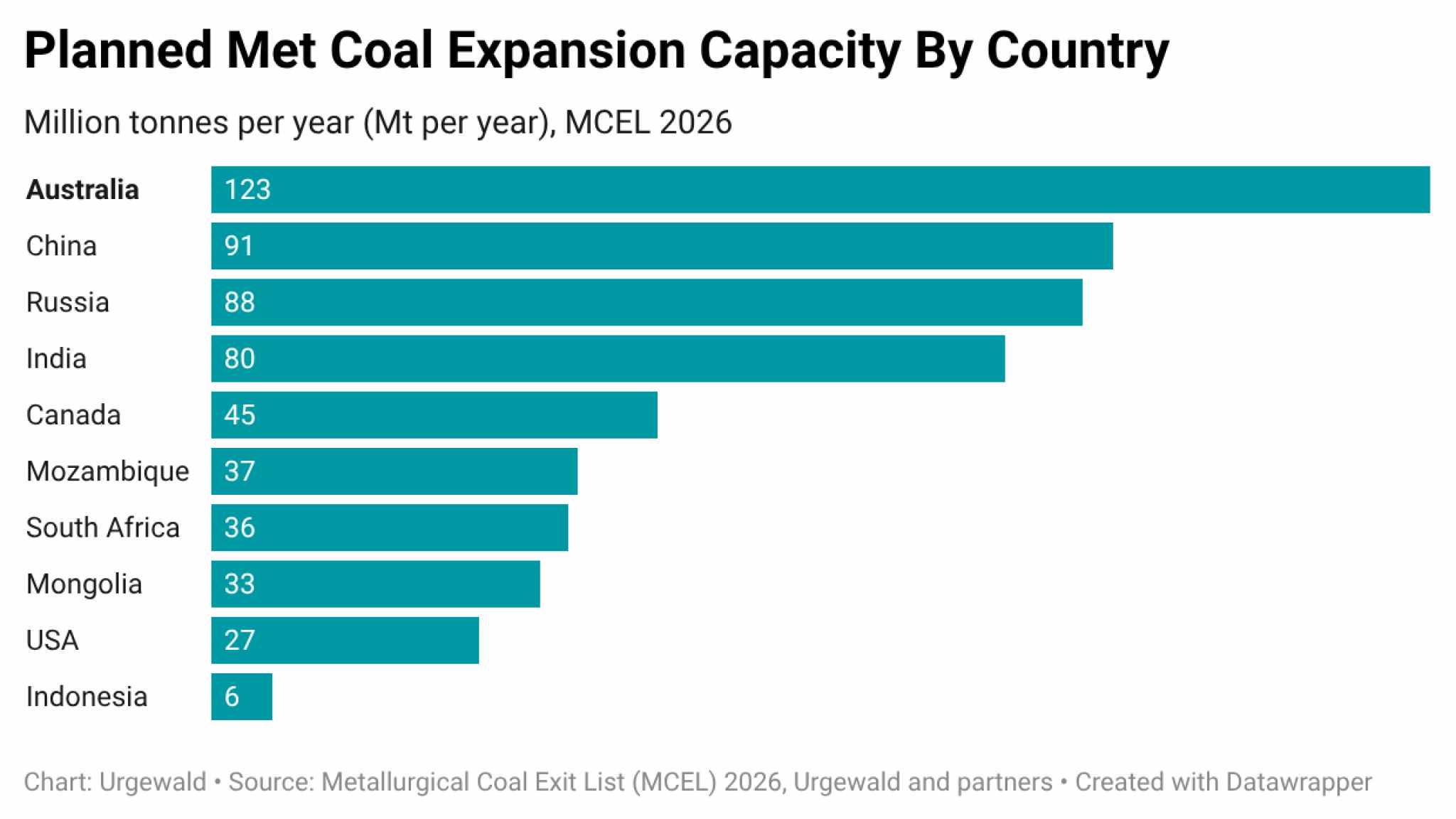

Urgewald’s new MCEL identifies 123 million tons per year[8] of planned expansion capacity in Australia, more than in any other country. (Figure 2)

The impacts on Australia’s environment are devastating. Much of this expansion is concentrated in eastern Australia, especially in the coal-rich state of Queensland, where open-cut mines push deeper into fragile bushland ecosystems and wildlife habitats.

Figure 2: Shows planned metallurgical coal expansion capacity by country, in million tonnes per year, based on MCEL 2026 data. Australia accounts for the largest share of planned expansion at 123 Mt per year, followed by China (91), Russia (88), and India (80). Canada (45), Mozambique (37), South Africa (36), Mongolia (33), and the USA (27) also show substantial planned increases, while Indonesia has the lowest planned expansion at 6 Mt per year. Source: MCEL 2026, Urgewald and Partners

The Moranbah South mine, planned and developed by Anglo American and Exxaro Resources, is the largest proposed pure met coal project, with an annual production capacity of 18 million tons.[9] Moranbah is located in Queensland’s Bowen Basin, one of the world’s largest coal mining regions. Anglo American is a UK-headquartered mining multinational, while Exxaro Resources is a major South African mining company. On its own, this volume would supply around 80% of the coal needed for Germany’s primary steel production.[10][11]

Yet, early warning signs of a downturn are already visible in Australia.

BHP is one of the world’s largest mining companies, with deep roots in Australia’s coal industry. Yet even BHP is being forced to confront the downturn. After announcing 750 job cuts in its metallurgical coal segment[12], the company has now scrapped plans for the Saraji East mine in central Queensland, an area that remains a vital habitat for native wildlife.

If it had gone ahead, Saraji East would have cleared koala habitat around 1,160 hectares, equivalent to around 1,600 football pitches[13], further pushing pressure on koalas already endangered in Queensland.[14][15]

Coal mining giant BHP is not alone. Another major Australian coal producer, Whitehaven, is also starting to pull back. Headquartered in New South Wales and expanding rapidly in Queensland, Whitehaven has been forced to shelve its approved Blackwater North project in the Bowen Basin, which would have boosted production and locked in mining until 2085.

But the pullback is not a clean break. Whitehaven is still moving ahead with construction at Blackwater South, a greenfield mine that would generate over 1.5 billion tons of carbon emissions from burning the coal, alongside millions of tons of methane released from the open pit. It also risks piling further pressure onto landscapes and ecosystems already under strain across Queensland’s coal regions.[16]

The strain is spreading beyond the biggest names. Pure play met coal companies are already taking hits: Coronado Global Resources posted losses in 2024[17] and was later downgraded with a negative outlook, while Bowen Coking Coal entered voluntary administration in 2025.[18] Both point to the same forces closing in: lower coal prices, rising production costs, and high government royalties.

How Trump’s Coal Obsession Blocks Progress

Not all countries are moving in the same direction. This year, the US administration designated metallurgical coal as a “critical raw material,” following Donald Trump’s Executive Order on “Reinvigorating America’s Beautiful Clean Coal Industry.”[19]

One of the key figures pushing this decision is Randall Atkins, CEO of Ramaco Resources. His company is now driving a new wave of mining under the banner of national security.[20] The Kentucky-based met coal miner is planning eight new met coal mines in the Appalachian Mountains. By claiming to “produce the materials that keep America strong,” the coal industry is repackaging environmental destruction as security policy.[21]

Harry Manin, Industrial Transformation Campaign Lead from US-based Sierra Club:

"Domestic steelmaking is important to our national economy and clean energy supply chain, but metallurgical coal is not 'essential.' In fact, met coke isn't needed at all. Billions of dollars are already being invested in the U.S. in Direct Reduction technology that completely eliminates coal-based pollution in steelmaking. The Trump administration's push to subsidize a 300-year-old method instead would lock in outdated practices. It will hobble American competitiveness globally and contribute to thousands of deaths locally."

Canada’s Elk Valley: Deformed Fish, Selenium Pollution, and Mountaintop Removal Mining

Beyond market risk, met coal expansion continues to carry major local environmental consequences. Metallurgical coal mining is also booming in Canada, but at a huge cost to the environment.

One of the most glaring examples is Elk Valley, a coal mining region in southeastern British Columbia, close to the border with Alberta, where mines sit upstream of communities and waterways that flow into larger river systems. Rivers in the affected region now contain fish with deformed skulls and twisted spines, the result of elevated selenium levels. Selenium is a naturally occurring element, but mining can release it into waterways at harmful concentrations, where it builds up in the food chain over time.[22]

One of the companies responsible for this disaster is Elk Valley Resources, a subsidiary of the Swiss mining giant Glencore. Glencore is one of the world’s largest mining and commodities companies, with global operations that stretch from coal and metals to large scale trading. Glencore employs one of the most destructive forms of coal extraction: Mountaintop Removal Mining (MTR). Still permitted in parts of the US and Canada, this method involves blasting off entire mountaintops to expose coal seams.

The resulting debris is dumped into nearby valleys and waterways, creating so called “valley fills.” These valley fills can permanently bury streams and change how water moves through a landscape, leaving a long-term legacy of contamination and habitat loss.

In British Columbia’s Elk Valley alone, Glencore operates four active MTR mines that together produce more than 20 million tons of coal each year. This production is concentrated in a landscape of steep mountain valleys, forests, and sensitive river habitats, where pollution travels far beyond the mine boundaries. The coal extracted from these sites has a greater climate impact than the total annual greenhouse gas emissions of the rest of British Columbia combined.[23]

Now, Glencore’s proposed expansion into Castle Mountain threatens important habitat for Rocky Mountain bighorn sheep and wide-ranging wildlife including grizzly bears.[24] Castle Mountain is also part of a wider ecosystem corridor where animals depend on large connected habitats, and new industrial development will fragment the landscape and increase pressure on already vulnerable species.

For more than half his life, Casey Brennan has lived along the Elk River, witnessing first hand how pollution has transformed the waterway. For residents like him, the harm is not only visible in the landscape, but in the loss of trust that clean water and a healthy environment will be protected for the next generation.

Casey Brennan, Elk River resident, comments:

“Financial institutions chase short-term profits, while our communities are left with the long-term consequences. Supporting Glencore means supporting an irresponsible system that undermines the region's ecological and financial health. The damage to water resources will last not just for decades, but for centuries. While private companies profit today, society will be forced to shoulder the costs for generations to come.”

In 2016, under pressure from Urgewald, Deutsche Bank and Commerzbank adopted explicit exclusions for MTR financing. Despite this, both banks provided around $5 million USD each to Glencore between 2022 and 2024.[25]

Heffa Schuecking, Director of Urgewald, said:

“This is a clear violation of the banks’ policies and sheds a dim light on their environmental due diligence. Banks cannot claim climate leadership while continuing to bankroll one of the most destructive forms of coal mining.”

UBS shows a similar gap between words and action. Despite pledging not to fund Mountaintop Removal Mining, UBS channeled around $7 million USD to Glencore over the past three years, making it Glencore’s biggest bank backer among peers in our dataset. In the Elk Valley, that money translates into real world harm: polluted rivers and devastated mountain ecosystems.

Metallurgical coal must no longer slip through the cracks of banks’ coal policies. It carries the same destructive footprint as thermal coal, and financial institutions must treat it with the same level of scrutiny and exclusion.

What MCEL 2026 shows

MCEL 2026 shows an industry in denial. Even as demand forecasts point to a decline in metallurgical coal this decade, companies are still lining up new mines across 20 countries as if the market will keep growing forever. The result is a global pipeline of projects that risks locking in decades of pollution, while creating a wave of high carbon assets that could quickly become stranded and worthless.

For communities living near these mines, this is not just a question of market risk. It means more land cleared, more water polluted, and more pressure on ecosystems that cannot be restored once they are gone. For banks and investors, it is also a test of credibility. Metallurgical coal can no longer be treated as a hidden corner of the coal sector. Financial institutions and policymakers have a clear choice: keep financing expansion that makes no economic or climate sense, or align decisions with the transition that is already underway.

Note to editors

MCEL 2026

The Metallurgical Coal Exit List (MCEL) is the world’s most comprehensive public database of of met coal developers. It is updated annually by Urgewald.

What MCEL tracks

MCEL 2026 identifies companies with planned new metallurgical coal mines and metallurgical coal mine expansions, including projects under development, in permitting, and not yet in operation.

Key metrics

The 273 expansion projects identified in MCEL 2026 represent around 580 million tons per year of planned new and expanded metallurgical coal production capacity.

Data and methodology

MCEL 2026 is based on publicly available company documents, regulatory filings, credible third-party sources, and specialist research.

A detailed methodology can be found here.

Additional information and project level detail are available on request.

About Urgewald

Urgewald e.V. is an environmental and human rights organization that has been campaigning for over 30 years to expose environmental destruction and human rights abuses linked to corporate and financial actors.

_________

- https://files.sciencebasedtargets.org/production/files/Financial-Instit…

- https://www.ilmarinen.fi/media_global/liitepankki/ilmarinen/sijoitukset… p.7

- https://iea.blob.core.windows.net/assets/113a8274-500c-4684-951f-947d25…

- https://iea.blob.core.windows.net/assets/113a8274-500c-4684-951f-947d25…

- https://icapcarbonaction.com/en/news/china-officially-expands-national-…

- https://hydrogen-central.com/chinas-hbis-to-supply-green-steel-to-italy…

- https://iea.blob.core.windows.net/assets/113a8274-500c-4684-951f-947d25…

- Please note that he availability of information and data on expansion capacity varies significantly across regions

- https://www.qld.gov.au/environment/management/environmental/eis-process…

- https://worldsteel.org/data/world-steel-in-figures/world-steel-in-figur…

- https://www.eurofer.eu/assets/publications/archive/archive-of-older-eur…

- https://www.reuters.com/world/asia-pacific/bhp-suspend-operations-cut-j…

- Football pitch equivalent calculated by converting hectares to square metres and dividing by a standard pitch area of 105 m × 68 m (7,140 m²). 1,160 ha equals 11,600,000 m², which equals around 1,624 pitches, rounded to around 1,600.

- https://www.koalasnotcoal.org.au/bhp_mitsubishis_saraji_east

- https://www.abc.net.au/news/2025-11-27/bma-drops-queensland-saraji-east…

- https://www.movebeyondcoal.com/whitehavens_blackwater_south_coal_mine

- https://announcements.asx.com.au/asxpdf/20250220/pdf/06fq7wgdgzgdcx.pdf

- https://www.abc.net.au/news/2025-07-30/bowen-coking-coal-appoints-admin…

- https://www.whitehouse.gov/presidential-actions/2025/04/reinvigorating-…

- https://ramacoresources.com/wp-content/uploads/2025/03/EE-News-Article-…

- https://ramacoresources.com/

- https://e360.yale.edu/features/from-canadian-coal-mines-toxic-pollution…

- https://www.banktrack.org/project/elk_valley_resources_metallurgical_co…

- https://wildsight.ca/2025/07/25/revised-fording-river-mine-expansion-st…

- https://www.urgewald.org/sites/default/files/media-files/Urgewald%20-%2…